Multivariate Gaussian Distribution

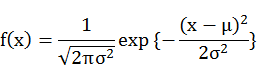

Random variable x follows normal distribution with mean μ and variance σ2,

denoted as x ~ G(μ, σ2). The density function is

denoted as x ~ G(μ, σ2). The density function is

and

The density function could be rewritten as

Consider the joint distribution with a vector-valued random variables X=(x1,…xn)T.

The density function of multivariate Gaussian distribution (MVG) with mean vector μ and variance-covariance matrix Σ.

The density function of multivariate Gaussian distribution (MVG) with mean vector μ and variance-covariance matrix Σ.

Further, Consider Y=AX+C if X ~ MVG(μ,Σ), and A, C are constant matrix.

No comments:

Post a Comment